Lisa : Right from the beginning. When you give stock to someone who works for you, the value of the stock is taxable, assuming that stock is vested at grant or if unvested at grant, is the subject of an 83 b election , just like if you give cash to someone who works for you. But when you give a person cash, some of that cash can be used to pay taxes. Stock options give recipients more choice and more flexibility, particularly with a company that has an uncertain future.

One thing you can clearly point to is when a company has actually raised venture capital and sold preferred stock in a priced financing round. These decisions are very nuanced and fact-dependent, so you have to be careful to look at the specifics of the company and its position at the time and get advice on this point.

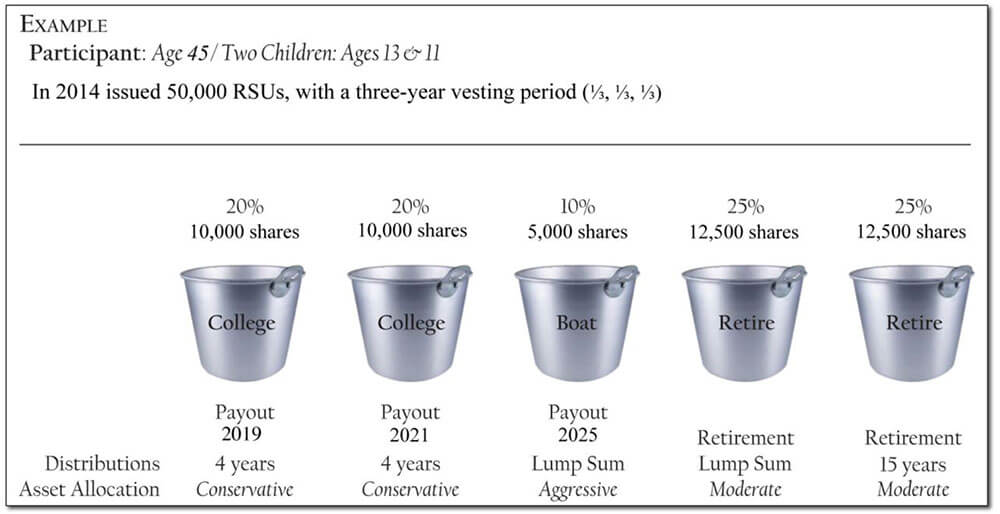

#1. Restricted Stock Units (RSUs) are a way your company can compensate you with stock

Lisa : When you grant stock options to employees, there are no taxes on the options at the time of grant. Exercising stock options does involve some risk, because it requires cash to buy the shares and, in some cases, to pay the tax based on the difference between the value of the stock at the time of exercise often based on a A valuation and the exercise price. Still, the stock option gives an employee a lot of flexibility to choose whether she wants to reduce her risk. She can either hold on to the stock options, not exercise them and just wait for an exit event to simultaneously exercise and sell her shares, or, she can exercise her stock options at any time before an eventual exit to try to get into a better tax treatment where she might possibly yield higher gains if the company has a successful exit event.

Lisa : The tax consequences vary depending on the type of option that the employee holds and can be pretty complex. On the other hand, if she exercised her stock options before the exit, she may be able to pay lower taxes if all goes as she hopes. If the value of the stock is greater than her exercise price when she exercises, she may owe tax on that gain, depending on the type of option she holds and her own personal tax circumstances. If the value of the stock increased over time and she was able to sell at a gain, this all means an overall lower tax obligation for her.

By exercising and trying to pay less in taxes and ultimately make more money, the employee is taking on risk though. That can be a big pain in the neck at really highly valued companies.

At these higher valuations, companies start to think about alternatives like RSUs restricted stock units. You just have the right to receive the value of a share of stock upon the occurrence of certain events. With restricted stock, you own the stock outright and if you met the statutory holding periods when you sell the stock, you get long-term capital gains treatment on the gain. You only receive stock and start your holding period for long-term capital gains purposes when the RSU vests.

Lisa : An RSU is really a promise for an employee to get a share of stock or sometimes, its cash value in the future.

Related Case Studies

RSUs have been around for a long time in public companies, and in a public company, they typically just have time or service-based vesting. Like I said before, when you get shares of stock from your employer, you owe tax on that. Your taxes will be based on the value when the RSUs vest and are converted into shares that you own.

One way private companies have gotten around this problem is to require an exit event for the RSUs to vest. The taxable amount will be the fair market value of the shares issued to you at vesting. Your restricted stock units shall become null and void if you do not execute and return the joint election form to your employer or to EA.

Therefore, before you decide to participate in the offer, you should carefully consider the fact that employer NICs will be payable by you at the acquisition of the shares when the restricted stock units vest, whereas they may not have been payable by you at exercise of your UK-approved eligible options or unapproved eligible options. You should refer to the relevant stock option agreement to determine whether the employer NICs liability was transferred to you in connection with your eligible options.

Sale of Shares.

Stock Options and Restricted Stock

You will be taxed on the difference between the sale proceeds and the fair market value of the shares at vesting. Please note that, effective April 6, , taper relief was abolished. If you hold the shares issued upon vesting of the restricted stock units, you may be entitled to receive dividends if EA, in its discretion, declares a dividend. Any dividend paid with respect to the shares will be subject to income tax but not NICs in the U. Your applicable tax rate will depend on your total income. You will need to declare your dividend income to HMRC on your annual tax return.

Build a custom email digest by following topics, people, and firms published on JD Supra.

You may be entitled to a tax credit against your U. If, for any reason, your employer is unable to withhold the income tax under the PAYE system or by another method permitted in the applicable award agreement, you must reimburse your employer for the tax paid within 90 days of the date on which the restricted stock units vest and shares are issued to you. If you do not reimburse your employer for the income tax paid on your behalf within 90 days of the acquisition of shares pursuant to the restricted stock units and assuming you are not a director or executive officer of EA within the meaning of Section 13 k of the Exchange Act , you will be deemed to have received a loan from your employer in the amount of the income tax due.

The loan will bear interest at the then-current HMRC official rate and it will be immediately due and repayable and your employer may recover it at any time by any of the means set forth in the award agreement.

Your employer is also required to report the details of the exchange of the eligible options, the grant and vesting of the restricted stock units, the acquisition of shares and any tax withheld on its annual tax returns filed with HMRC. You are also responsible for paying any tax resulting from the sale of your shares and the receipt of any dividends.

The following is a general summary of the material UK tax consequences of the voluntary cancellation of eligible options in exchange for the grant of restricted stock units pursuant to the Offer to Exchange for eligible employees who were tax resident and ordinarily resident in the United Kingdom when they received the eligible options they elect to cancel in the exchange but who have subsequently relocated outside the United Kingdom before they receive restricted stock units in the exchange. You likely will not be subject to UK income tax or NICs as a result of the exchange of eligible options for the grant of restricted stock units pursuant to the Offer to Exchange.

Notwithstanding that you have relocated outside the UK, you will be subject to UK income tax when the restricted stock units vest and shares are issued to you if:. However, HMRC is generally prepared to reduce the UK tax liability to reflect the relative number of workdays that you have spent in the UK and the other country between grant and vesting of the option and the subsequent grant and vesting of the restricted stock units except where there is a relevant tax treaty between the UK and your new country of residence which provides otherwise.

Getting ESOP as salary package? Know about ESOP Taxation

If you are subject to tax in the UK and your new country of residence on the same income, you may be able to apply for a tax credit in respect of the UK tax liability in your new country of residence. We strongly recommend that you check with your tax advisor to confirm whether double taxation applies and whether it may be possible to reduce your tax liability in the other country based on the tax paid in the United Kingdom.

If you have not relocated on a permanent basis, your liability to UK employee and employer NICs will depend on your personal circumstances and you should consult your personal tax advisor. In addition, EA may require you to assume the employer NICs due on the income realized at vesting of your restricted stock units. To accomplish this, you may be asked to execute a joint election, and your restricted stock units may be cancelled if you do not execute and return the joint election form to your employer or to EA.

However, please note that EA is not in a position to assure you of this outcome and EA may not be able to obtain confirmation from HMRC prior to your decision to exchange the options or the vesting of the restricted stock units. We strongly recommend that you check with your tax advisor to confirm whether you may be subject to social security contributions on the income in both countries and whether you will be able to avoid such double taxation. Subject to the provisions of any relevant double taxation treaty, you may also be subject to capital gains tax in the United Kingdom when the shares acquired are subsequently sold even if you are no longer in the United Kingdom at the time of sale.

Please see above for general comments on capital gains tax on the sale of shares. Please consult your tax advisor, as the tax treatment of a transferring individual into or out of the United Kingdom is often complex and will depend upon your particular circumstances.

- KPMG Personalisation.

- Vesting RSUs and RSAs?

- binary options brain.

- How to Report RSUs or Stock Grants on Your Tax Return - TurboTax Tax Tips & Videos?

- trading system volatility breakout;

- the best swing trading system.

- Got investments??

The comments regarding Dividends above will apply to you if you are resident in the UK at the time at the time any dividends are paid but not otherwise. Withholding and Reporting.