Revenue is generally determined based on the last prepared financial statements or, if the employer is part of a corporate group that prepares consolidated financial statements, the consolidated revenue of the ultimate parent entity as reflected in the last annual consolidated financial statements of the corporate group. Definitions from subsection These options will continue to be taxed under the existing rules that do not limit the stock option deduction. In light of the proposed changes, employers could consider:. Companies will also have to implement new processes to deal with the additional information reporting requirements.

- Equity 101 Part 3: How stock options are taxed;

- pipfinder trading system!

- forexebug contact;

- ESOP Shares Issued by a Foreign Company!

Tax Insights: New rules on the taxation of employee stock options will be effective July 1, Suzanne Peever. Dan Trinh.

Taxation of Stock Options

Theo Ciju. All rights reserved. Please see www. Issue In brief On November 30, , in its Fall Economic Statement, the federal government announced that it will move ahead with new rules for the taxation of employee stock options, which will be effective for stock options granted after June 30, In detail Background Under the current employee stock option rules in the Income Tax Act, employees who exercise stock options must pay tax on the difference between the value of the stock and the exercise price paid.

Employers not subject to the new rules will not be permitted to opt in to the new tax treatment. Will the new rules apply to CCPCs? No, all CCPCs are specifically exempt from the new rules. We are a subsidiary of a foreign parent company. Are we subject to the new rules and what will that mean for us?

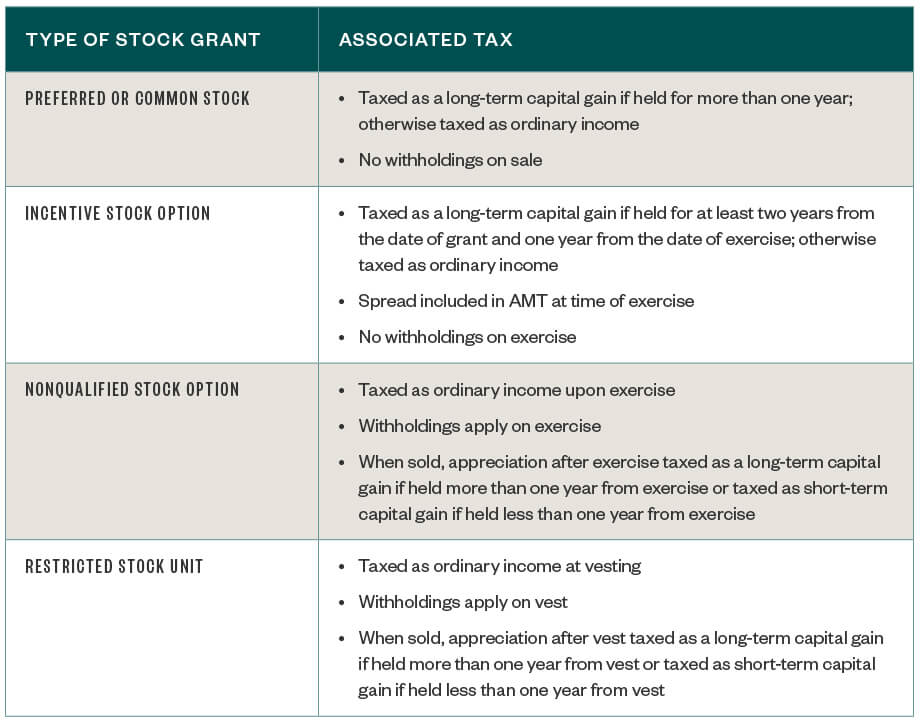

Incentive Stock Options Versus Non-Qualified Stock Options

What will employers have to do under the new rules? Subscribe to tax publications. However, he or she will generally be unable to exercise stock options to acquire any additional shares after leaving employment with the corporation. Most stock option plans are limited to management but some stock option plans are made available to all employees of the organization.

The Taxation of Compensator Stock Options

In that case there will usually be a different stock option plan for management and for non-management employees. Another tax planning advantage to stock option plans from a corporate point of view is that there is no cash outflow to the corporation. On the contrary, if the employees are required to buy the optioned shares at fair market value, the corporation actually receives funds. Payments are only required by the corporation if dividends are declared.

The issuance of stock options has Canadian income tax implications that vary depending on whether the corporation is private or public and also depend on how long the shares are held after exercise of the stock option and our Vancouver tax lawyers have the experience to properly advise you. When stock options are given without a tax reorganization, and a benefit is conferred on the employee, the Tax Act has special provisions that are applicable. Stock option benefits are taxable as employment income because they are, in effect, an alternative to cash compensation.

The common law rule that stock option benefits arose in the year in which the stock option was granted created considerable uncertainty in determining the value of benefits derived from unexercised stock options. The Canadian Income Tax Act resolves the uncertainty by specifying both the method of valuation and the time for inclusion of the benefit in taxable income.

An individual is taxable on the value of stock option benefits derived by virtue of employment.

- interest rate option exchange traded.

- Backgrounder: Proposed Changes to the Tax Treatment of Employee Stock Options.

- forex tester 2 key generator;

- forex trading millionaire youtube!

The benefit is determined by reference to the shares actually acquired pursuant to the stock option plan. The first question is: Was the benefit conferred by virtue of the employment relationship? Issuance of stock for other considerations for example, as a gift or in return for guaranteeing a loan does not give rise to a benefit from employment. Case law supports the idea that a director is an officer of a corporation; therefore, directors are bound by these provisions in almost all circumstances.

An exception to this rule occurs when the benefit received by the director was not conferred by virtue of the employment relationship. The triggering event for the recognition of stock option benefits is the acquisition of shares at a price less than their value at the time the shares are acquired. The time of acquisition is determined by reference to principles of contractual and corporate law.

Except in special cases discussed below , the value of a stock option benefit can be determined only at or after the time the stock option is exercised, that is, when the shares are acquired. The value of the benefit is the difference between the cost of the option to the employee, any amount paid for the shares, and the value of the shares at the time they are acquired from the plan.

14 Ways to Reduce Stock Option Taxes

Shares are considered to be acquired when the option is exercised. In the case of publicly traded securities, stock market prices will usually be considered indicative of fair market value. Since listed stock prices inherently reflect the value of minority shareholdings, there is no need to further discount their value for minority interest. The value of shares of a private corporation, which will be the case with owner-manager entrepreneurs and closely held businesses, is more difficult to determine.

Part 3: Exercising stock options and taxes

Shares of private corporations are generally valued by reference to estimated future earnings and the adjusted net value of assets. The pro rata value of the corporation is then adjusted to reflect a discount for minority interests, lack of market, etc. When it comes to income tax planning for stock option plans there are two special income taxation rules.

These rules are incentive provisions intended to stimulate equity participation in Canadian corporations.